Date:

December 29, 2025

Author:

Anastasia Fainberg

/

Founder & Managing Partner

A full year can pass faster than we expect. You blink, and you’ve lived twelve months of school drop-offs, work deadlines, snowstorms, sick days, birthdays, and the ordinary busyness that makes Denver life feel full.

And somehow, the retirement plan you meant to “tighten up” is still sitting in the same place it was last year. Not because you don’t care. And not because you’ve been irresponsible.

It’s because retirement planning often feels like it belongs in the “someday” category, right next to updating your estate plan, checking beneficiaries, and having the conversations no one feels excited to start.

Then January shows up again. New year. High hopes. Resolutions. A quiet voice that says: This is the year I get it together.

Here’s the question I want you to consider, calmly, without pressure: What if this is the year you actually put the plan together?

Because in Colorado, a retirement account isn’t just a savings vehicle. For many families, it’s the largest financial promise you’ll ever leave behind.

And the part that controls whether that promise turns into protection, or into confusion and unnecessary taxes, often comes down to a single, easily overlooked detail:

Your beneficiary designations.

In this article, I’ll explain why retirement accounts can create hidden traps for Denver families, how the SECURE Act changed inherited IRA timing, and what a clear, protective structure can look like in 2026, especially if you’re raising kids, supporting aging parents, navigating a blended family, or trying to make sure your hard work doesn’t get drained by avoidable mistakes.

Why Retirement Accounts Can Derail Colorado Estate Planning (Even When You Have A Will)

A retirement account is not just “money in an account.” It’s a contract. It has its own rulebook. And it often ignores the rest of your plan if the beneficiary form doesn’t match your intent.

Here’s what I see over and over in Colorado families: your IRA beneficiary form outranks your will, even if your will is beautifully written.

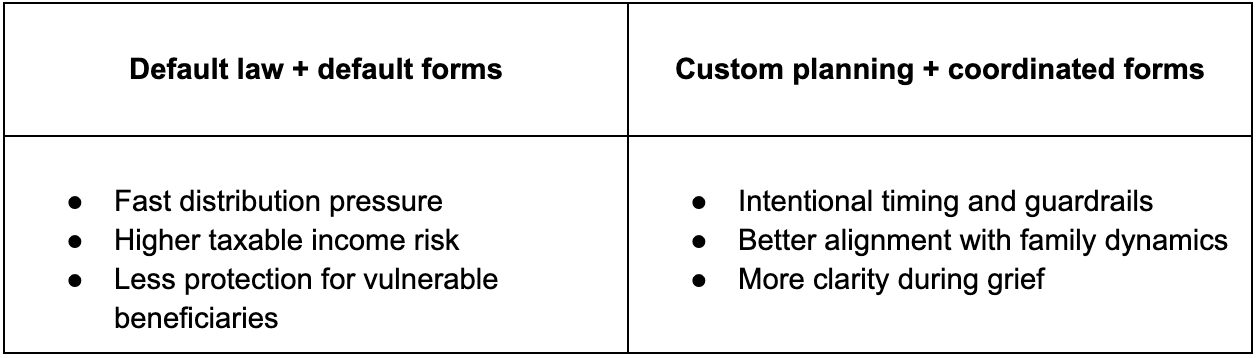

The SECURE Act created a tighter timeline that can push inherited IRAs into higher tax brackets faster. The IRS has been clarifying inherited RMD expectations, final rules apply for calendar years starting in 2025, which matters for 2026 planning.

Blended families are where “simple” beneficiary choices can become emotionally complicated. Naming minors directly can trigger court involvement, delays, and expensive workarounds.

Pro Tip: If you’re searching Denver will attorney or will attorney near me, ask whether your planning includes a retirement-beneficiary audit, not just documents.

Case Study: Mark

Mark lived in Centennial. Two kids from his first marriage. A remarriage later in life. A paid-off home, a solid career, and a large traditional IRA that represented decades of discipline.

His intent was simple: “When I’m gone, my wife is okay, and my kids still inherit.”

So he named his spouse as the primary beneficiary. And he named the two kids as contingent beneficiaries, “50/50.”

On paper, that looks fair. In real life, it created a trap.

When Mark died, his wife had full control over the inherited IRA path. She wasn’t a bad person. She was grieving, overwhelmed, and trying to keep life stable. But the retirement rules, the tax timing, and the family dynamics put pressure on every decision.

The result wasn’t a “family inheritance moment.” It was years of stress, and a tax hit the kids didn’t see coming.

That’s why I call retirement planning a form of legacy planning. If the structure is wrong, the consequences don’t show up in your lifetime. They show up in your children’s.

What The Secure Act Changed For Inherited Iras (And Why It Matters In 2026)

Before 2020, many families planned around the idea of a “stretch IRA,” where children could take smaller distributions over a longer life expectancy.

The SECURE Act changed the default rhythm for many non-spouse beneficiaries.

In plain English, for many inherited retirement accounts, the money generally must be distributed within 10 years.

And the IRS has made it clear that for certain situations, especially when the original owner died after their required beginning date, annual RMD expectations may apply during years 1–9, not just a lump sum in year 10.

Yes, there has been transition relief for certain years and fact patterns. But the direction is consistent: inherited retirement accounts are meant to move faster than many families assume.

That matters because faster distributions can mean higher taxes, especially for adult kids in their peak earning years.

And for many in Denver, the family story often includes multiple layers at once: kids, aging parents, second marriages, and real estate responsibilities. (For context, per the US Census Bureau, Denver’s population is growing and shifting, and about 12.3% of Denver residents are age 65+, meaning more families are actively navigating retirement-era planning right now).

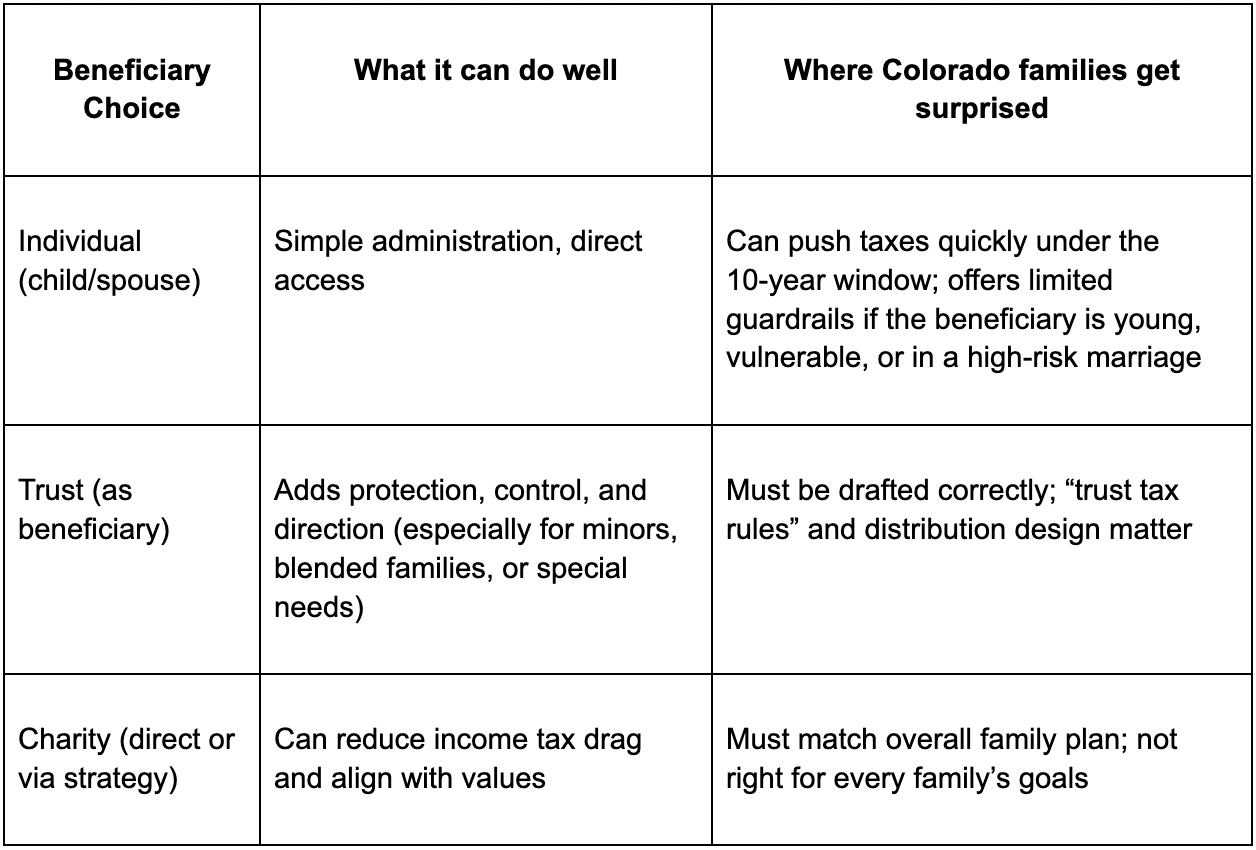

Individual Vs. Trust Vs. Charity: When A Trust Attorney Helps You Choose The Right Ira Beneficiary

This is where a trust attorney earns their keep. Because “Who do I name?” is not just a names question. It’s a timing question. A tax question. A protection question.

Here’s a simple comparison I use with clients:

If you’re a small business owner with a solo 401(k), SEP IRA, or large retirement balance, this is especially important. Your retirement account may be one of your most liquid assets, and the easiest one to accidentally misdirect.

The Quiet Emotional Cost Of Getting This Wrong

When retirement accounts are structured poorly, families don’t just “pay more tax.” They lose clarity.

A surviving spouse wonders if they’re allowed to spend what they need. Adult children worry they’ll look greedy if they ask questions. Stepchildren feel like outsiders in a story they were promised they belonged in.

And in Colorado, where so many families are blended, mobile, and juggling care across cities (Highlands Ranch to Lakewood, Centennial to Cherry Creek), uncertainty spreads fast.

As a mom and as a daughter, I think about this differently than a spreadsheet does.

Your plan is supposed to remove pressure from your family, not add it.

Key Retirement-And-Trust Concepts Colorado Families Should Understand

Beneficiary Designation

This is the form that controls who inherits the retirement account, often more powerful than your will.

Eligible Designated Beneficiary

A category the IRS recognizes (like a spouse, minor child, disabled or chronically ill individual, or someone not more than 10 years younger) that may allow different payout treatment.

The 10-Year Rule

A common SECURE Act framework requiring many inherited retirement accounts to be fully distributed within 10 years, which can accelerate taxes.

Required Beginning Date (RBD)

A timing marker for the original owner that can change whether annual distributions are expected for heirs.

“See-Through” Trust Planning

A trust can be an IRA beneficiary, but it must be drafted and administered properly to align with federal retirement rules and your family’s goals.

Special Needs Planning

If a beneficiary receives means-tested benefits, the wrong inheritance structure can threaten eligibility, this is where a special needs trust attorney search is often the beginning of a very important conversation.

The Reality: The Irs Has A Timeline If You Don’t

Here’s the bottom line I want Denver families to hear clearly:

If your retirement account beneficiary choices don’t match your planning goals, federal rules will still apply on a timeline that may not be emotionally or tax-friendly for your family.

Common Misconceptions (Myths)

Myth #1: “My kids inherit retirement accounts tax-free.”

Most inherited traditional retirement distributions are taxable income to the beneficiary. The question is often how fast and how much at once.

Myth #2: “My will controls my IRA.”

In most cases, your beneficiary designation controls your IRA, not your will. That’s why estate planning has to include forms, not just documents.

Myth #3: “I’ll leave it to my spouse and they’ll share.”

Many spouses intend to share. But “intent” isn’t enforceable unless the structure makes it enforceable, especially in blended-family situations.

Myth #4: “Trusts always cause higher taxes.”

Trusts can be designed in different ways. The real issue is matching the trust design to your goals: protection, timing, tax efficiency, or a blend.

Myth #5: “This is only a problem for wealthy families.”

I see this in solid middle and upper-middle income Denver households all the time, because retirement accounts are often the largest pool of “transferable” wealth.

Why This Really Matters (And What I Want For Your Family)

When you set a 2026 goal, you’re not just setting a number. You’re setting a direction.

Retirement accounts are part of your family’s safety story. They’re meant to fund dignity for a spouse. Opportunity for children. Stability during loss.

And when those accounts are mishandled, families don’t just lose money, they lose calm.

As I often tell families, it’s not about money. It’s about the people you love.

How To Start In 2026: What To Ask An Estate Planning Attorney About Ira Beneficiaries And Trusts

- Pull your beneficiary designations for every IRA and 401(k) you have.

- List your “real-life family” realities: remarriage, minor kids, special needs, uneven financial maturity, caregiver dynamics.

- Match each account to your goal: spouse security, kid protection, tax efficiency, or all three.

- Review how your trust is drafted (if you have one) before naming it on a beneficiary form.

- Coordinate your plan with your CPA/financial advisor, then make sure the legal structure supports the tax strategy.

- Schedule a Retirement & Tax Strategy Review with a Denver estate planning attorney using our LIFT approach (Legal, Insurance, Financial, Tax).

FAQs (Colorado Families Ask These Every Week)

Does naming beneficiaries avoid Colorado probate?

Retirement accounts with named beneficiaries typically pass outside probate, but that doesn’t mean they’re automatically protected or tax-efficient.

Can a trust be the beneficiary of my IRA?

Yes, but it needs to be designed correctly. This is where a living trust attorney can help you avoid accidental consequences.

What if my beneficiary is a minor?

Naming a minor directly often creates court and practical complications. A trust-based approach can add control and reduce chaos.

What are “eligible designated beneficiaries”?

The IRS includes categories like a surviving spouse, the account owner’s minor child, a disabled or chronically ill individual, or someone not more than 10 years younger.

Will my kids have to empty the inherited IRA in 10 years?

Many non-spouse beneficiaries fall under the 10-year rule, and the details can depend on timing and status.

Are there situations where annual inherited RMDs matter before year 10?

Yes, especially when the original owner died after their required beginning date; IRS guidance has addressed annual distribution expectations in certain cases.

Does a Roth IRA have the same inheritance tax issue?

Roth distributions are often tax-free if rules are met, but the 10-year distribution window can still apply, which affects timing and planning.

What if I want to include charity in my plan?

Charitable planning can reduce income-tax drag in certain situations and align giving with legacy goals, but it should be coordinated with the rest of your family plan.

What should I ask my estate planning attorney in the first meeting?

Ask whether they review beneficiary designations, understand SECURE Act inheritance timing, and can coordinate a trust strategy with your tax professional.

Closing Reflection

If 2026 is your year to get organized, don’t stop at contributions and account balances.

Make sure your retirement accounts actually reach the people you love, on purpose, with protection, and with as little tax friction as your situation allows.

Don’t leave your family’s future to chance. Schedule your consultation with Legacy Law Group Colorado today and take the first step toward peace of mind.